Real estate accounting plays a crucial role in the real estate industry, with nearly 10 million people in the United States owning rental properties. Over 50% of these property owners hire a property manager to handle their accounting needs, underscoring its importance (source: Strategic Market Research).

Understanding Real Estate Accounting

Understanding the basics of real estate business accounting is crucial for assessing your company’s financial health and ensuring tax compliance. Accurate accounting enables you to make informed decisions about your properties.

While real estate accounting seems complex, mastering the basics is essential for success in the field. For instance, knowing your maintenance expenses and having your go-to service vendors allows you to plan more effectively for future repairs.

This guide provides the foundational knowledge to get you started, offering a solid understanding of real estate accounting.

What is Real Estate Accounting?

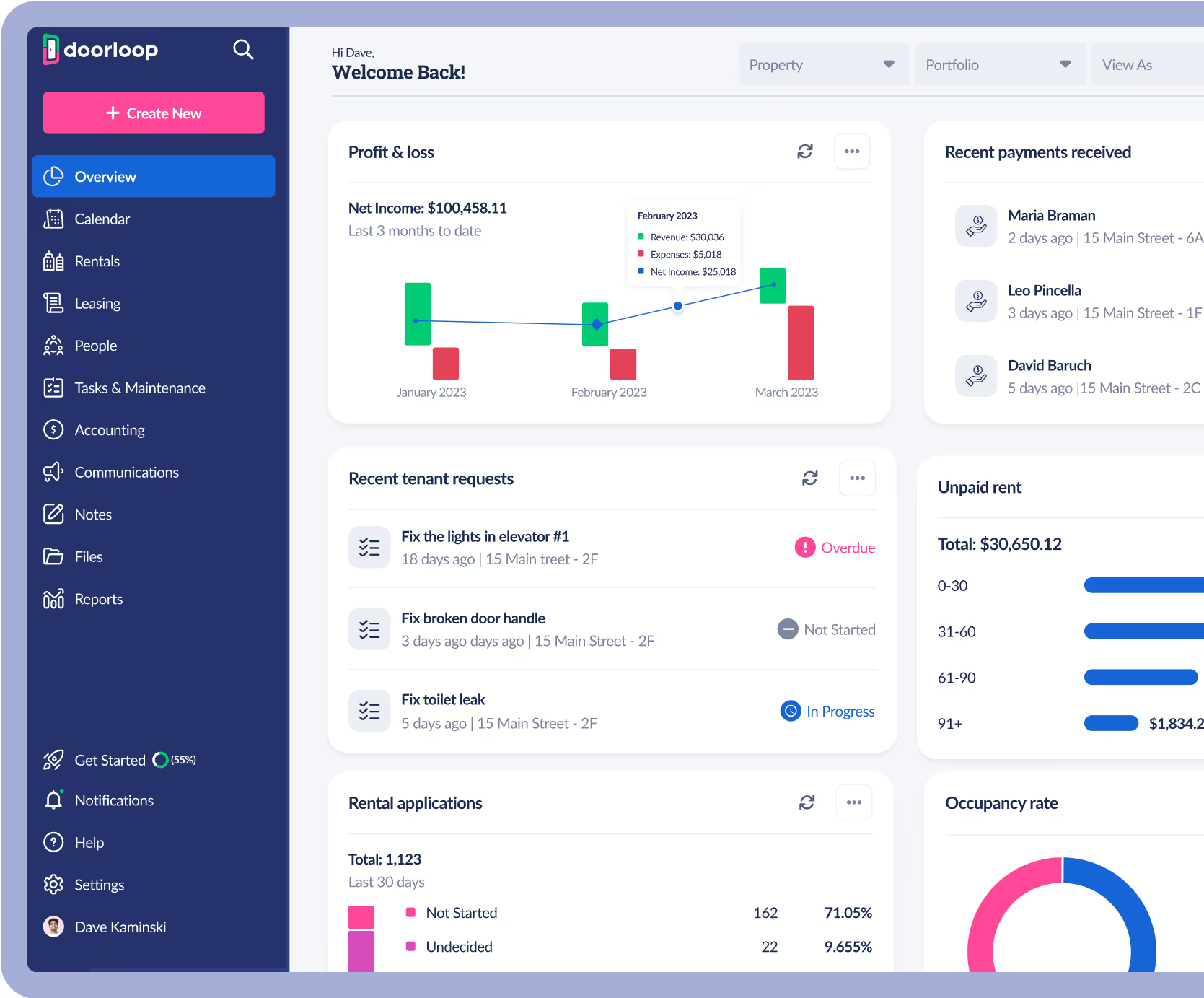

Real estate accounting is the process of keeping track of all the money that comes in and goes out related to real estate properties. This includes everything from the rent you collect from tenants to the expenses you have for repairs and maintenance. Implementing a comprehensive real estate accounting system can help improve cash flow, control income and expenses, and monitor property performance.

Real estate accounting involves several crucial activities from tracking income and expenses, to tax preparation and account reconciliation to budgeting and financial planning.

Difference Between Accounting and Bookkeeping

Believe it or not, these practices are different and are often mistakenly interchanged. Each has a distinct function and purpose. Let’s clear up some of the confusion.

- Bookkeeping: Focuses on the accurate recording of all financial transactions. This includes tracking purchases, sales, receipts, and payments. Bookkeepers ensure that records are up to date and provide a clear financial picture at any given time.

- Accounting: Goes beyond bookkeeping to analyze, interpret, and report financial data. Accountants create budgets, study financial trends, and develop strategies to increase profits and reduce expenses. They provide insights that help guide business decisions.

Roles and Responsibilities:

- Bookkeepers: Handle day-to-day financial tasks and ensure that the company’s books are balanced. They are responsible for maintaining accurate records, tracking transactions, and ensuring that financial data is organized.

- Accountants: Focus on the bigger financial picture and long-term planning. Accountants analyze the financial data recorded by bookkeepers to create comprehensive reports. They advise on financial planning, tax compliance, and business strategies.

Key Components of Real Estate Accounting

Income From Commissions

Real estate agents generate income from property sales and commissions associated with each closed deal.

You should always accurately track, monitor, and report all incoming sources of cash.

Expenses and Deductions

There are may deductions and expenses that you can claim, which is why we alway recommend speaking with a CPA, but here are 5 important ones:

- Association Fees and Expenses: Includes fees paid to brokerages and professional associations.

- Office-related Charges: Office supplies, rentals, and maintenance services.

- Marketing Expenses: Costs related to promoting properties, such as website design, social media management, and advertisements.

- Continuing Education Costs: Expenses for maintaining licenses through education.

- Travel, Mileage, and Transportation Expenses: Costs for visiting properties and meeting clients.

Best Practices for Real Estate Accounting

Separating Personal Funds from Business Funds

Keeping personal and business finances separate is essential for effective real estate accounting. This separation simplifies your financial management and ensures compliance with tax regulations. Separating personal and business funds is crucial for accurately analyzing your business's financial performance.

Why It’s Important:

- Clarity: Separate accounts provide a clear picture of your business’s financial health without personal expenses complicating the view.

- Compliance: Keeping business transactions distinct helps in accurate tax reporting and reduces the risk of errors.

- Credibility: Maintaining separate accounts builds trust with clients and financial institutions.

How to Do It:

- Open Separate Bank Accounts: Open a dedicated corporate bank account for your real estate business to manage income and expenses.

- Use Business Credit Cards: Utilize business credit cards for all business-related purchases to keep transactions distinct.

- Set Clear Boundaries: Avoid using business funds for personal expenses and vice versa to maintain financial integrity.

Something else to consider when opening a corporate bank account is to potentially open multiple business accounts and using each one for specific business purposes. For example, one account is only used to pay debts where another account is solely used for marketing and promotion expenses.

The key here is to only use the account for its intended purpose and never use one account to fund the other. If using multiple corporate accounts, calculate what percentage of business income will go into each corporate bank account.

Accurate Reporting Procedures

Accurate data is also very important for generating various financial reports, such as profit and loss statements and income statements. Automated software helps streamline this process.

Itemizing Transactions

Properly itemizing your transactions saves time and effort during tax season. Familiarize yourself with IRS Schedule E for relevant deductions and categories.

Monthly Reviews

Conducting regular financial check-ups is essential. Reviewing your accounts monthly helps you keep track of income and expenses.

Learn Local Requirements

Understand and comply with local tax regulations and business requirements. This knowledge will help you avoid fines and ensures your business operates within legal guidelines.

Backup Financial Data

Regularly back up your financial data to prevent loss, and consider using technology platforms with cloud storage for this task. This ensures you have access to past information for tax filings and audits.

Communicate with Financial Professionals

Maintain clear communication with your accountant, bookkeeper, and other real estate professionals so everyone is informed of any changes and can provide the necessary support.

Basic Steps in Real Estate Accounting

Choose an Accounting Method

In real estate, you can choose between cash basis or accrual basis accounting:

- Cash Basis: Records money when it is actually received or paid.

- Accrual Basis: Records money when it is earned or spent, even if not yet received or paid.

Create a Chart of Accounts

A chart of accounts categorizes all financial items in your business, including assets, liabilities, income, and expenses. It helps you organize and understand your finances better.

- Assets: Shows all the value of a business like your cash, property, and money owed.

- Equity: Keeps track of the owner's contributions and shares.

- Expenses: Money lost from buying anything, paying bills like taxes, vendors, repairs, utilities, and any business costs.

- Liabilities: Used for money you might owe back like security deposits.

- Revenue: Money earned from rent, management fees, etc.

Track Important Real Estate Transactions

Monitor key transactions, such as brokerage fees, overhead costs, and vendor expenses. Keeping detailed records is crucial for tax preparation and compliance.

Organize Documents

Develop a filing system for managing business-related documents. Keeping organized records ensures you have a clear overview of all transactions and can quickly access information when needed.

Reconcile Accounts

Ensure your account balances are accurate by reconciling them monthly. Review transactions in detail and set up automated reminders to keep your books up to date.

Common Real Estate Accounting Mistakes

Accounting is hard, which is why making mistakes is so common. Unlike other mistakes in other business areas, an accounting mistake can be detrimental.

Here are some specific errors to watch out for:

Failure to Back Up Files and Data

Regularly back up your financial data to prevent loss due to technical issues or unforeseen events. Use cloud storage or external hard drives to ensure you have access to your records when needed.

Lumping Expenses Together

Avoid combining all expenses into broad categories. Itemize expenses to provide accurate records and maximize tax benefits. This helps in identifying specific cost areas and ensures you take advantage of all available deductions.

Not Waiting for Funds to Clear

Do not rely on commission checks or other payments until they have cleared. Prematurely spending funds can harm your cash flow if deals fall through. Wait for confirmation before using these funds for expenses or investments.

Mixing Personal and Business Finances

Keep personal and business finances separate by using dedicated bank accounts and credit cards for your real estate business. This prevents confusion, ensures accurate record-keeping, and simplifies tax preparation.

Inaccurate Record-Keeping

Ensure all transactions are recorded accurately and promptly. Use accounting software to track income, expenses, and other financial activities to maintain precise records and facilitate easy audits.

Ignoring Local Tax Regulations

Stay informed about local tax regulations and compliance requirements. Failure to comply can result in fines, penalties, and legal issues. Regularly review updates and consult with a tax professional to stay compliant.

Real Estate Accounting Glossary

Frequently Asked Questions

Is real estate accounting difficult?

Real estate accounting can be complex due to the need for accurate tracking of income, expenses, tax compliance, and financial reporting. However, with the right tools and knowledge, it can be managed effectively. Many real estate professionals use accounting software or hire accountants to simplify the process.

What accounting method do realtors use?

Realtors typically use either the cash basis or accrual basis accounting methods. Cash basis accounting records income and expenses when they are actually received or paid. Accrual basis accounting records income and expenses when they are earned or incurred, regardless of when the money is received or paid.

What is real estate bookkeeping?

Real estate bookkeeping involves recording and tracking all financial transactions related to real estate activities. This includes documenting income from rent and sales, expenses for maintenance and operations, and preparing financial statements. Bookkeeping ensures that accurate financial records are maintained for tax preparation and financial analysis.

What is real estate fund accounting?

Real estate fund accounting refers to the specialized accounting practices used to manage and report on real estate investment funds. It involves tracking the financial performance of a portfolio of properties, managing investor contributions and distributions, and ensuring compliance with regulatory requirements. Fund accounting focuses on providing detailed financial information to investors and stakeholders.

.svg)

.svg)